Here’s an interesting little debate from earlier this year that I came across yesterday evening. It is between a number of market analysts over whether the current stock market is overvalued. Why is that interesting? Because the argument is focused on one of the best known foundational stones of heterodox economics: the Levy-Kalecki profit equation.

Weird? Not really. James Montier, a well-known investment analyst at GMO, has been using the profit equation as central to his forecasting work for a number of years. You can see his latest offering here (page 5). Montier’s argument is that profits in the US at the moment are heavily reliant on the still rather large budget deficits that are being run there. I made a similar argument on the Financial Times Alphaville blog over a year ago.

This is actually a non-controversial point. Private sector savings are equal, to the penny, to the budget deficit minus net imports. This is intuitively obvious: when the government spends money that money either accrues to a private sector institution within the country or to a foreigner abroad. We then divide the private sector into households and firms and we quickly see that budget deficits are equal, again to the penny, to net imports, household savings and… you got it: profits.

All of this is just basic accounting. The above cannot be in any sense ‘untrue’ because this is how the accounting apparatus works. So, why is David Bianco from Deutsche Bank disputing this? Basically he confuses an accounting identity with a behavioral equation. He writes:

This construct assumes that no savings are recycled as investment. This is not a small matter. It represents a major conceptual flaw in this framework, which taints the entire analysis. The equation above would only be correct if all savings were stuck in a Keynesian liquidity trap.

Um… no. It does not assume that. The above equation says nothing with regards to how an increase in savings will effect the level of investment. It is just an accounting identity. As Keynes’ protege Joan Robinson argued many years ago in her book An Introduction to Modern Economics (co-authored with John Eatwell):

For purposes of theoretical argument we are interested in causal relationships, which depend on behavior based on expectations, ex ante, whereas the statistics necessarily record what happened ex-post… An ex-post accounting identity, which records what has happened over, say, the past year, cannot explain causality; rather it shows what has to be explained. Keynes’ theory did not demonstrate that the rate of saving is equal to the rate of investment, but explained through what mechanism the equality is brought about. (pp216-217)

If Bianco were clearer about what he was arguing he would say something like this:

“Montier may be correct on the accounting but he is wrong on the causality. An increase in savings by firms and households will lead to an increase in investment by those same firms and households.”

This is, of course, the mainstream (pre-Keynesian) argument that assumes that, as savings increase, interest rates fall across the board and investment increases.

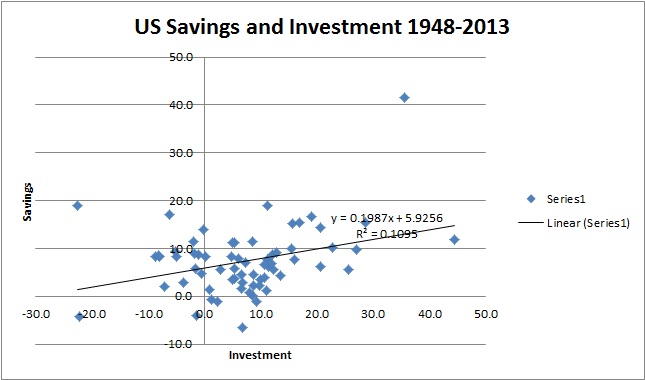

Note that this is a causal argument. At the point in Montier’s analysis when he summons Kalecki, he is not making a causal argument. He is just stating accounting facts. But Bianco’s argument implies that when we see increases in savings in the economy we should also see increases in investment. Does the data reflect this? Short answer: no. Below is a regression plotting gross private savings against gross private domestic investment (all data from FRED).

As you can see, the relationship is extremely weak. If I were Bianco I wouldn’t be buying stocks based on a causal argument that yields an R-squared of 0.1095.

But perhaps, it will be argued, it takes a while for the savings to transmit into investment. Nope. If we lag the investment variable by a year the outcome is even worse: we get a slightly downward-sloping line (negative relationship) with an R-squared of 0.0022.

Even more interesting is if we turn to the past 15 years. In the above regression we can at least see a positive correlation between the two variables, however weak that might be. But if we take the last 15 years we see a negative correlation implying that as savings increases/decreases investment decreases/increases.

We even get an R-squared that is a bit higher than the first regression — although I’d be somewhat reticent to bet the house on it.

Now, some people with some basic macro training may be a little confused about all this. After all, doesn’t savings equal investment? Isn’t this an identity that we are taught in the first pages of our macro textbook? This is, after all, precisely what Bianco complained about when he wrote of Montier’s analysis:

This is neither the point of the argument nor the general condition, thus the [Kalecki] equation above fails to recognize that: Investment = Savings.

Given that the deficit is “forecast” by such august bodies as the Congressional Budget Office to decline significantly over the next few years, it will take either a remarkable recovery in investment spending or a significant re-leveraging by the household sector to hold margins at the levels we have witnessed of late. Thus, embedding such high margins in a valuation seems optimistic to me.(p4)

“Corporations are currently using the cash they are accumulating to engage in share buybacks”

That does beg the question what are the people receiving the share buyback money doing with the money – given those tend to be, in the main, pension funds, etc.

Share buybacks are just dividends paid to people who don’t want to hold the share any more (!).

Transitively there has to be at the end of the cash chain an entity that is hoarding monetary savings, or reducing the size of bank balance sheet somewhere.

I love the piece but just a minor issue, which might be either my mistake or yours:

“Budget deficits are equal, to the penny, to private sector savings minus net imports.”

Should this sentence not read, “Budget deficits are equal, to the penny, to private sector saving minus net EXPORTS”?

Or, alternatively, “Budget deficits are equal, to the penny, to private sector savings PLUS net imports.”?

Sorry, if I am being pedantic

No. Minus net imports. Or, plus net exports.

Exports add to savings. Imports subtract from savings.

Net imports means foreigners are accumulating savings.

The govt budget deficit must therefore be equal to domestic private sector net saving plus this accumulation of savings by foreigners.

So budget deficits should be equal to domestic private sector net saving plus net imports.

If the budget deficit is 100, and domestic private sector net saving is 50, then net imports must be 50, as foreigners are accumulating 50 in savings.

If on the other hand the budget deficit is 100, and private sector net saving is 150, then net exports must be 50, as the domestic private sector is accumulating savings by exporting abroad. In which case the budget deficit would be equal to domestic private sector net saving minus net exports.

Sorry Phil.

G-T is identical to S-I + M-X..

So a government deficit flows into increased domestic savings and/or to foreigners

Almost…

(T – G) = (I – S) + (X – M).

if there is a budget deficit, (T – G) will give you a negative number.

As it should…

If the govt spends 200 (G = 200) and taxes only 100 (T = 100), it runs a deficit.

The deficit is equal to (G – T) = (200 -100) = 100. Not -100.

I think you’re confusing the algebra with the interpretation. Equations only equate. They do not “say” anything.

in my example above the budget deficit is equal to 100. The budget surplus is equal to -100.

Yeah. The surplus is negative, if you want to look at it that way.

More straightforwardly: taxes minus expenditure is minus one hundred.

I think something is getting mixed up in your conceptual formulation right now, but MsJones described both the correct english explanation and the correct formula. Do a sanity double-check against the wiki: http://en.wikipedia.org/wiki/Sectoral_balances

Ooops. Above equation was wrong. Changed.

Original point still stands. Exports add to savings, imports subtract from savings. In algebraic form:

S = I + (G – T) + (X – M)

Compare with derivation in Wiki article:

(S – I) = (G – T) + (X – M)

Same thing.

Yep agreed that’s correct. The original point though was about your article’s description in english: “Budget deficits are equal, to the penny, to private sector savings minus net imports.”

That is saying that flow out of government sector is equal to flow into private sector minus flow into foreign sector. That’s either wrong or confusingly worded if the “minus” clause is supposed to be applied to the first term.

Not “foreign sector”. “Net imports”. So, minus the cost of net imports.

If the government runs a deficit of 100 and 80 is spent on goods produced at home while 20 is spent on good produced at home then it all balances. In formal terms we have said:

Private sector savings = government deficit – net imports

Same thing as I said verbally in the post.

“Private sector savings = government deficit – net imports”

That’s correct, but what you said in the post is:

“Budget deficits are equal, to the penny, to private sector savings minus net imports.”

which is incorrect.

Fixed.

makes sense now. Cheers.

Let’s restate this: net exports increase the amount of (foreign) money or foreign promises to pay (commercial credit) in a country, which counts as savings.

the goods exported are not consumed in the domestic economy, so the represent savings. The saving occurs both in real terms and in financial terms (foreign money or promises to pay).

*so they represent savings

Bianco is wrong from the start. Savings do not fund Investment. All Income = all Spending

Hence, if I save more (spend less) someone else’s income goes down and they will save less.

Instead, it is Investment which creates Savings. So the equation is correct but most have causality in the wrong direction.

Also the identity Savings = Investment holds, government or no government. As we know, a government deficit increases private savings but not, as pointed out, investment. However, in this case, the government is dissaving so the equation still holds. That is, Saving = Public Saving plus Private Saving.

Thanks.

the identity saving = investment holds for the global economy as whole, including governments. But it doesn’t necessarily hold in the single domestic economy, or for the private sector on its own.

“Given that corporations are currently using the cash they are accumulating to engage in share buybacks and given that the household sector has been rebuilding its balance sheet over the past few years after which we can only assume that they will be a tad more conservative in their borrowing”

Well, share buybacks add to profits like dividends do, don’t they? As for the household sector, I think you put the wrong link, but anyway, Steve Keen has posted some data which indicates that households are levering up again:

http://www.businessspectator.com.au/article/2014/3/31/economy/why-us-cant-escape-minsky

(the article is from March 2014)

So a cynical prediction would be that the current credit cycle still has a long way to go. I don’t know how many economists are predicting this sort of thing, though. (and I’m not an economist)