Yesterday I did a short post on how the ISLM model misrepresents how interest rates function because it views them as static. Today I would like to make a further, if more difficult point: namely, that the very way in which the interest rate stimulates investment is inherently limited in that it cannot produce cyclical upswings in effective demand — and thus, cannot produce cyclical upswings in output. In doing this I will be drawing on Jan Kregel’s excellent paper Of Prodigal Sons and Bastard Progeny which in turn draws on some of Joan Robinson’s own writings on the ISLM.

As Kregel shows in the paper, Robinson had a very clear-sighted view about how interest rates function. The first part of Robinson’s article is quoted by Kregel as such,

Relatively to given expectations of profit, a fall in interest rates will stimulate investment somewhat, and by putting up the Stock Exchange value of placements [i.e. share prices], it may encourage expenditure for consumption. These influences will increase effective demand and so increase employment… But even when the rate of interest can be moved in the required direction, it may not have much effect. The dominant influence on the swings of effective demand is swings in the expectation of profits. (My Emphasis)

Here then there are two channels through which a fall in the interest rate works. On the one hand, it increases investment directly — presumably by lowering the cost of borrowing somewhat and giving a temporary boost to the animal spirits. On the other, it increases consumption expenditure through the wealth-effect as the net worth of those that hold shares rises. The increase in effective demand then arises due to the increase in investment and consumption that arises due to the fall in interest rates.

However, as I highlighted in the above quote, Robinson takes a properly Keynesian/Kaleckian view of how such increases in investment may or may not prove self-reinforcing: that is, in order for a cyclical upswing to be maintained expected profits must increase. Robinson is skeptical that this will occur under the influence of monetary policy because she thinks that the fall in interest rates will lead to,

…a boom which will not last because after some time the growth in the stock of productive capacity competing in the market will overcome the increase in total expenditure and so bring a fall in the current profits per unit of capacity, with a consequent worsening of the expected rate of profit on further investment.

The increased investment creates a bigger pool of productive capacity which then competes in the market for profits. This, in turn, drags down the profit on each unit of productive capacity. Since profit expectations are now somewhat dampened and since the fall in the interest rate has run its course further investment will fall off and the boom created will fizzle out. In the book from which Kregel draws the quotes, Economic Heresies, Robinson makes crystal clear that this is the Keynesian view proper.

[Keynes’] account of a boom is to say that a high rate of investment causes a fall in expected profits as the supply of productive capacity increases… one thing he would have never have said is that a permanently lower level of the rate of interest would create a permanently higher rate of investment.

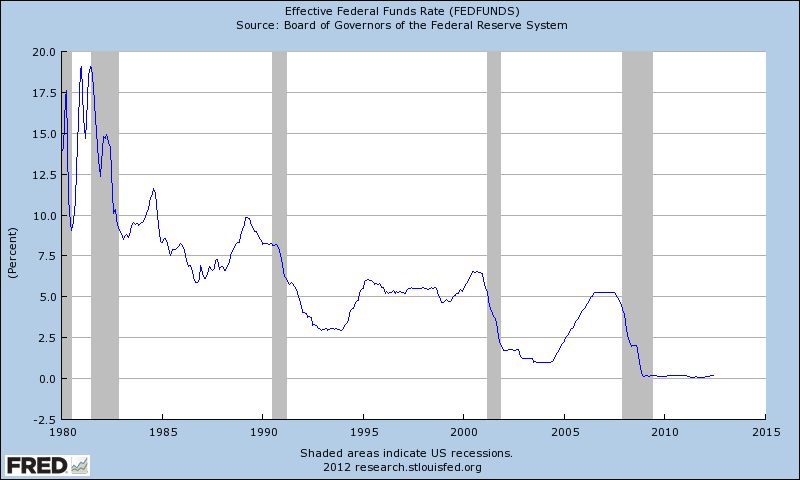

This ties into Kalecki’s argument that if central banks try to control the level of effective demand through the interest rate they will find that they will have to drop the interest rate over and over again as each boom peters out until, ultimately, they end up at the zero-lower bound. As Steve Randy Waldman of Interfluidity notes, this appears rather prescient if we look at the period after 1980 when central banks moved toward trying to steer the economy by using the interest rate alone. He presents the following graph which shows precisely this dynamic,

As we can see, after each recession the central bank had to drop the interest rate ever lower to ensure that an expansion could take place. This is precisely what Keynes, Robinson and Kalecki would have expected.

The problem here, as in my original post on the ISLM, is that its adherents do not seem to understand the difference between statics and dynamics. Kregel states this quite clearly, all the while drawing on Robinson,

[U]sing Hicks’ IS curve, “a permanently lower level of the rate of interest would cause a permanently higher rate of investment”. This Keynes “could never have said” for it confused equilibrium with a process of change: “Keynes’ contention was that a fall in the rate of interest relatively to given expectations of profit would, in favourable circumstances, increase the rate of investment”. But, this would cause expectations to change and the marginal efficiency of capital curve to shift, and presumably the IS curve with it. An IS schedule could not be built upon the static relation between interest and investment.

Where many Post-Keynesians, and even some New Keynesians like David Romer, today focus on the LM-curve when critiquing the ISLM framework, Robinson showed how the IS-curve was simply not compatible with Keynes’ own theory. At the same time she showed how it was inapplicable to any world in which investment was based on the expectation of future profits.

Again, we should emphasise the underlying problem here: the ISLM model is based on a static framework that simply cannot conceptualise dynamics. What is more, the framework is not some ‘provisional’ outline sketched out prior to a more sophisticated dynamic analysis; indeed, it cannot be as it falls apart under dynamic conditions. Nor are the misinterpretations it produces ‘innocent’ in the sense that the errors only exist in the abstractions of the model; it is quite clear that those who use the model will likely come to extremely wrong-headed policy prescriptions (the call for a negative rate of interest today as the cure of our ills being one that comes to mind…).

The ISLM discourages economists from thinking in the very manner that they should think: that is, in terms of the historical time in which we all live, historical time in which expectations formed under uncertainty are of the utmost importance. It trains economists into thinking that they are like social engineers who understand the economy as one might understand the functioning of a piston-engine. But economists are no such thing and any economist who convinces themselves otherwise will soon find themselves running headfirst into the double-glazed window that the rest of us call ‘reality’.

Addendum: For a further critique of the idea of using the interest rate to control economic fluctuations see here for a completely different but equally powerful and, I think, somewhat novel argument by your’s truly.

What about the simple point that Steve Keen makes – that IS/LM requires Walras Law to be in play in equilibrium before you can drop the labour market from the model.

I’m not sure that it’s so strong. ISLM is pretty explicit that it requires a flexible labour market to ensure full market-clearing. I think that ISLMists are well aware of this.

It’s more than that. Only Walras Law allows you to have only two curves on the diagram, or more specifically a single point.

Otherwise you *cannot* ignore the labour market, there must be three lines and that means you might not have a single point on the graph where all the markets overlap.

In other words the diagram is inconsistent under its own definition. (Debunking Economics, pp237)

The ISLM is seen as a short-run model. So, any increase in money or whatever lead to increased employment. The assumption is that something is stopping the labour market from clearing — i.e. the model requires that something is “holding up” the labour market.

In the long run, it is assumed that the labour market will clear. This is sometimes represented in the ISLM-FE model where the vertical FE line represents a full employment labour market:

ISLM-FE

Partially formed thought: If the Treasury and Central Bank were consolidated, can’t we look at the drop “beyond” the zero bound as just another way of saying that countercyclical spending is necessary?

I don’t follow… the suggestion above is that the interest rate is generally a terrible way of steering the economy no matter what. The implicit alternative is that we should always use fiscal policy to pull the economy out of recession.

This is confusing to me. From the Keynes/Kalecki/Levy macro profit identity, any increase in investment is also an equal increase in profits, all else equal, and the rate of profit must rise with investment if the capital stock depreciates over time. The issue must therefore be that all else is not equal, and an increase in investment is associated with higher household savings, higher fiscal balances, or lower current account balances (all “leakages”, hence reducing profit relative to investment in any accounting period). And so if we were to graph the marginal propensity to invest (or the inverse of Keynes investment expenditure multiplier, and sometimes mistakenly taken by early Keynesians as algebraic shorthand for the accelerator principle), which for Keynesian stability conditions, is less than the marginal propensity to save in aggregate investment/saving and aggregate income space, we should see a rising rate of profit and profit share as aggregate income increases and we approach the point of intersection of the two schedules, and then a falling profit share and profit rate as economic growth takes aggregate income out beyond the point of intersection, and into the area of the graph where the increase in nominal saving per increase in nominal income exceeds the increase in investment per increase in nominal income. Also, I recall in Accumulation, Robinson dealt with some of these nonlinearities in her infamous banana diagram, and Kaldor also, in his early theorizing about business cycle dynamics, used nonlinear investment and saving schedules. But I may simply be confused about all this, and now will go back and read the original Kregel article and approach him on some of this.

I think it’s pretty simple really. It’s tied to the old Domar problem.

Say there are ten machines with $500k keeping them running through pure consumption. Now investment increases by $250k producing ten more machines. Ignore savings by workers. Aggregate profits go up to $750k. But profits per machine fall from $50k to $37.5k.

Thus the expected rate of profit falls.

They’re very simple numbers. But I’d imagine you can do this in lots of ways. And then when you bring in productivity and longevity — Robinson’s “hard” versus “soft” ploughs — you find more and more of these Domarian problems arising.

BTW this ties into why I was arguing with Vernengo about the Harrod-Domar model versus the ISLM stuff on Facebook.

Frankly, I think a lot of Post-Keynesians — following the likes of Palley (I’m not blaming him, but its a trend) — have become fascinated with statics. It really is blinding them to the more important issues that Robinson and Kaldor highlighted back in the day. (And Harrod and Domar before them).

Many PKs today don’t seem to realise that, in “cleverly” creating new-fangled ISLMs and the like to accommodate aspects of PK theory, they are just taking a giant step backwards.

I think the Levy crowd have avoided this though (for now). And Bill Mitchell is including it in his new textbook.